Using the Adjusted Trial Balance to Amend the 1120-S Tax Return

See how the adjusted trial balance connects your books to your tax return. A real S-corporation walkthrough: clearing a tax payment, fixing a subsidiary error, combining entities, and converting to cash basis for Schedule M-1.

Financial accounting and tax accounting can feel like two separate worlds, but in real business they constantly meet. One of the places they meet most clearly is the adjusted trial balance. It does more than show where a company stands financially; it becomes the bridge between your books and your tax return. That link is especially important for S-corporations, where accurate financial reporting and careful tax compliance go hand in hand. Let us walk through how the two work together, using a real S-corporation example.

What the Adjusted Trial Balance Does

The adjusted trial balance is a summary of every account balance after you have entered all the necessary adjustments. Those adjustments correct any gaps in the original (unadjusted) trial balance and bring everything into line with accounting standards like GAAP or IFRS. Once they are in place, the adjusted trial balance shows the true closing balance of every account in the general ledger. That clean, corrected picture is exactly what you need before you prepare a tax return.

A Quick Word on S-Corporations

S-corporations are known for pass-through taxation, so it helps to be clear on what that means. Unlike a regular C-corporation, an S-corporation does not pay federal income tax on its profits. Instead, the profits and losses pass through to the shareholders, who report them on their personal returns and pay tax at their individual rates. The corporation itself may still owe certain state taxes, franchise taxes, or other local obligations, but federal income tax is handled at the shareholder level. Keep that in mind, because it drives the first adjustment below.

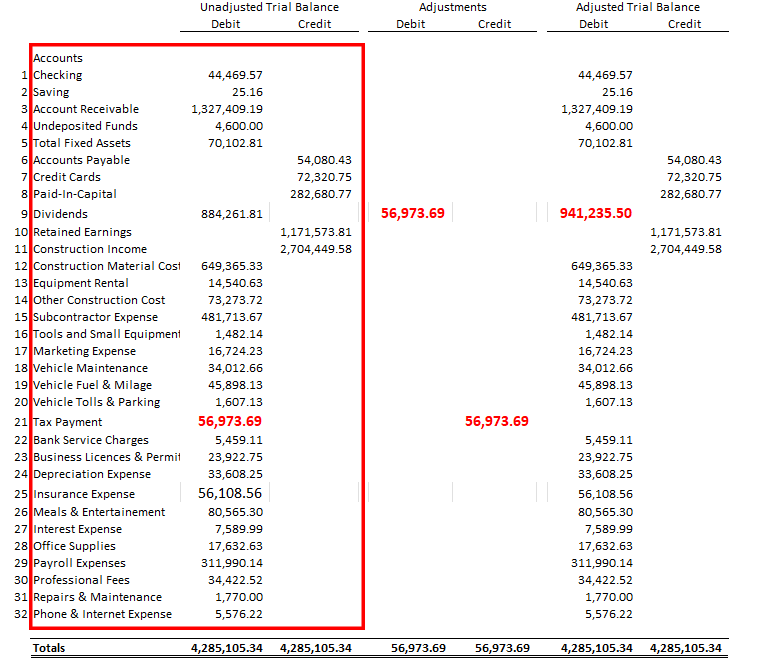

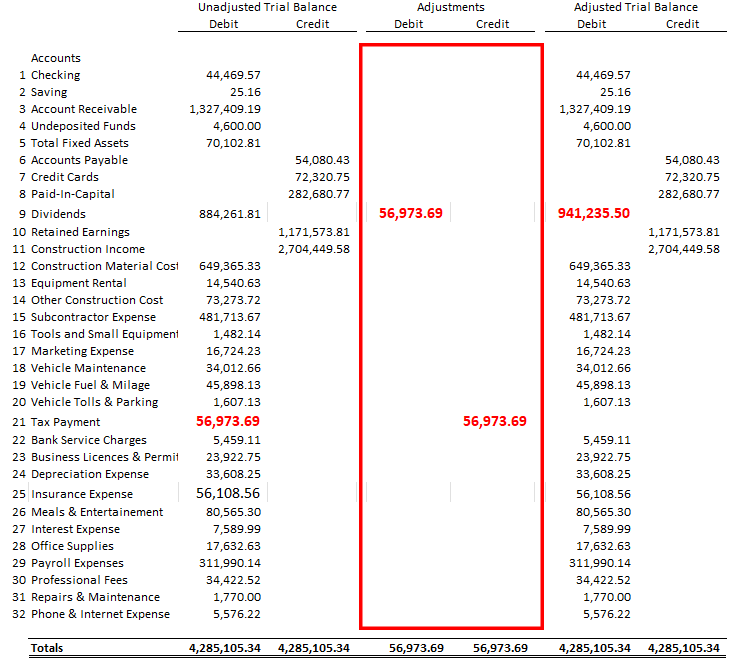

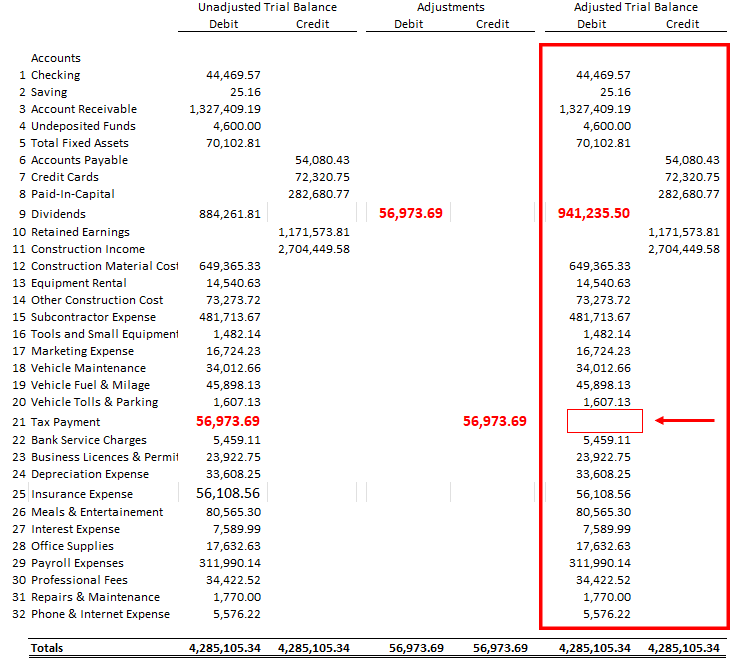

Part 1: Fixing a Tax Payment That Should Not Be There

When you look down the unadjusted trial balance, a problem stands out: a debit balance of $56,973.69 sitting in tax payments. For a pass-through entity, that figure should be zero, since the S-corporation does not pay federal income tax itself.

To correct it and stay compliant, you record one adjusting entry: a debit of $56,973.69 to Dividends and an equal credit to Tax. That single entry clears the discrepancy.

In the adjusted trial balance, Dividends rises by $56,973.69 to a total of $941,235.50, and the Tax Payment account zeroes out, exactly as it should for an S-corporation.

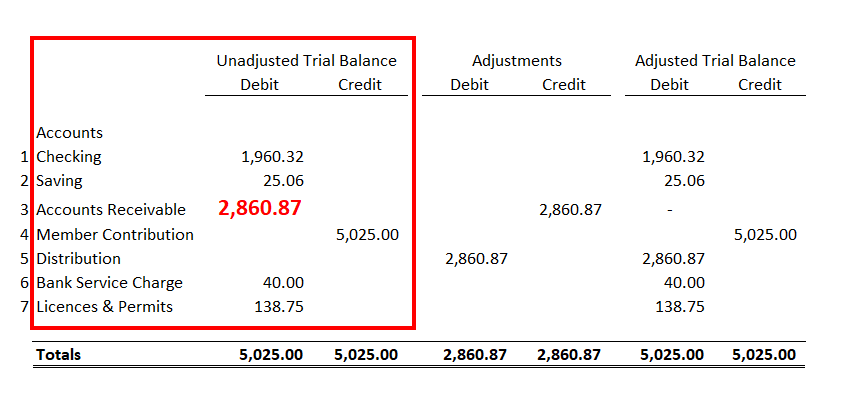

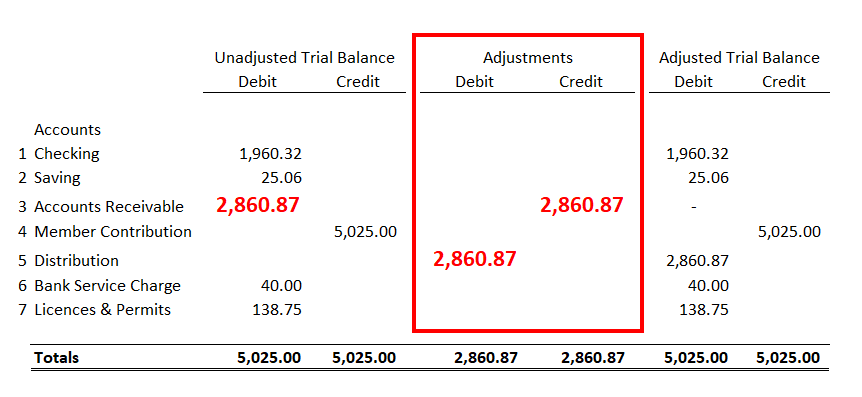

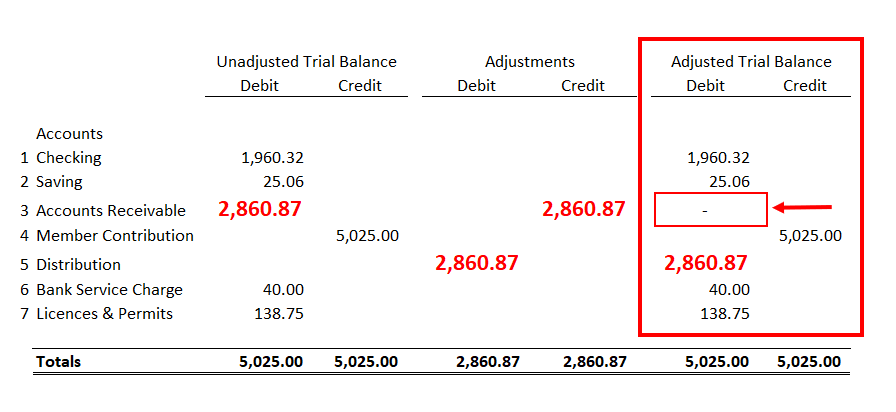

Part 2: Correcting an Error in a Subsidiary

Now imagine the company owns several subsidiaries set up as C-corporations. In one of them, a $2,860.87 debit was recorded by mistake in the Accounts Receivable line of the unadjusted trial balance.

To fix it, you record two entries: a $2,860.87 debit to Distribution and a $2,860.87 credit to Tax Payment.

After the adjustment, Accounts Receivable returns to zero and Distribution increases by $2,860.87 in the adjusted trial balance.

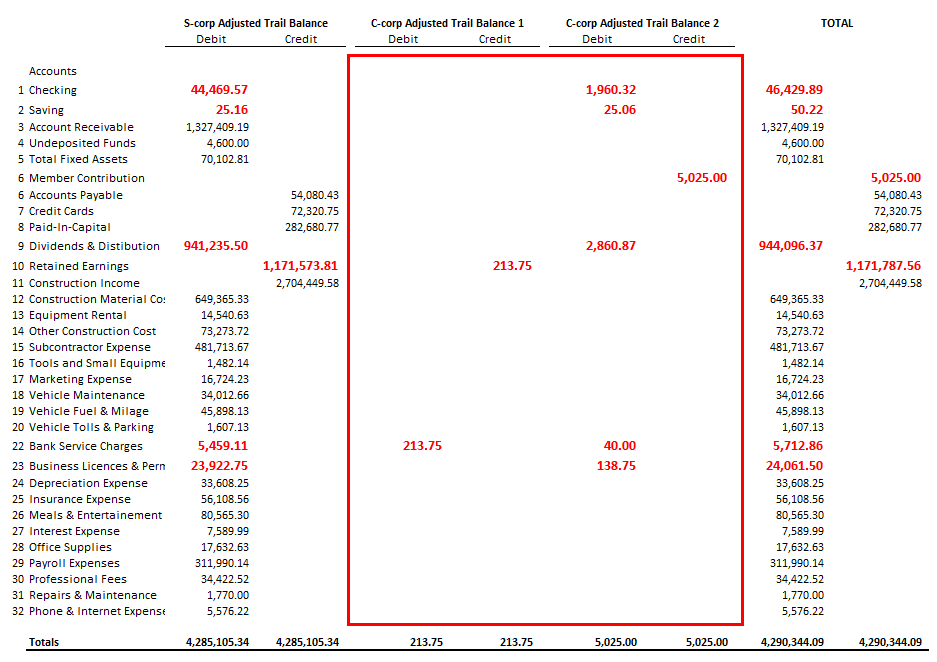

Part 3: Combining the Trial Balances

When you consolidate the trial balances of the S-corporation and its two C-corporations, the combined picture comes together like this:

- Checking increased by $1,960.32 and Savings by $50.22 on the debit side.

- Member Contribution shows a credit balance increase of $5,025.00.

- Dividends and Distribution together reflect the earlier $2,860.87 debit adjustment.

- Retained Earnings now show an increased credit balance of $213.75.

- Bank Service Charge increased by $253.75 on the debit side.

- Business License and Permits increased to a higher total debit balance of $138.75.

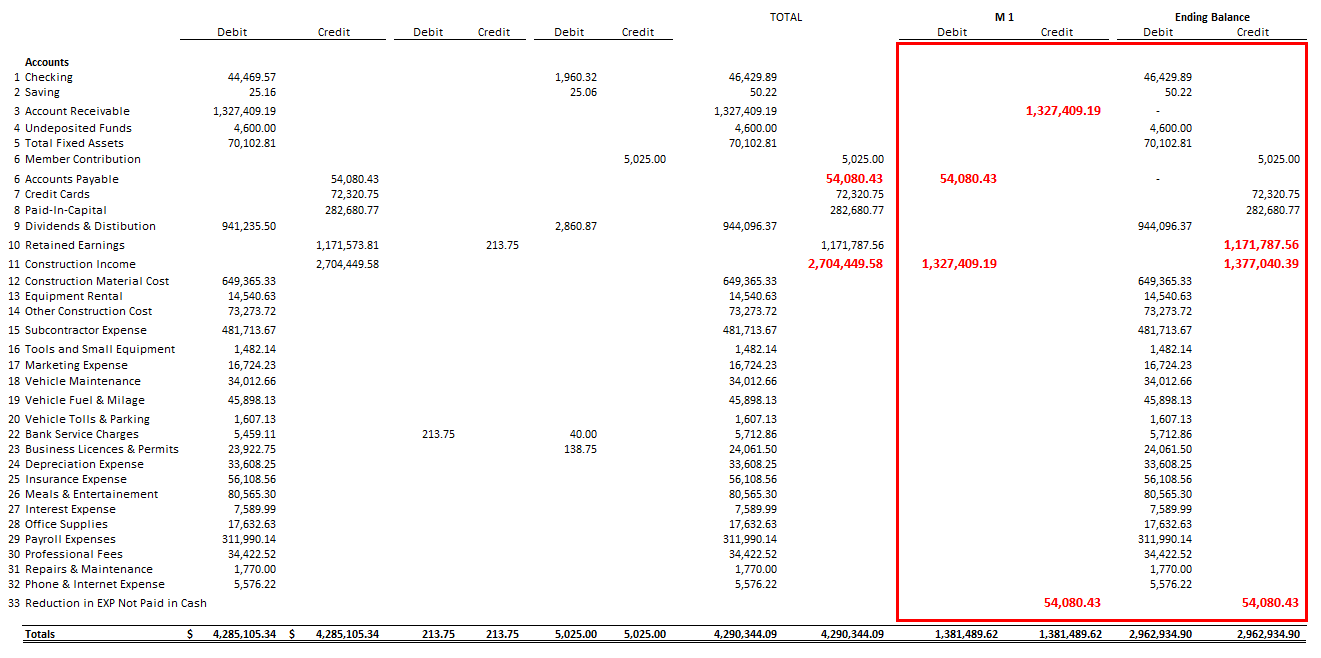

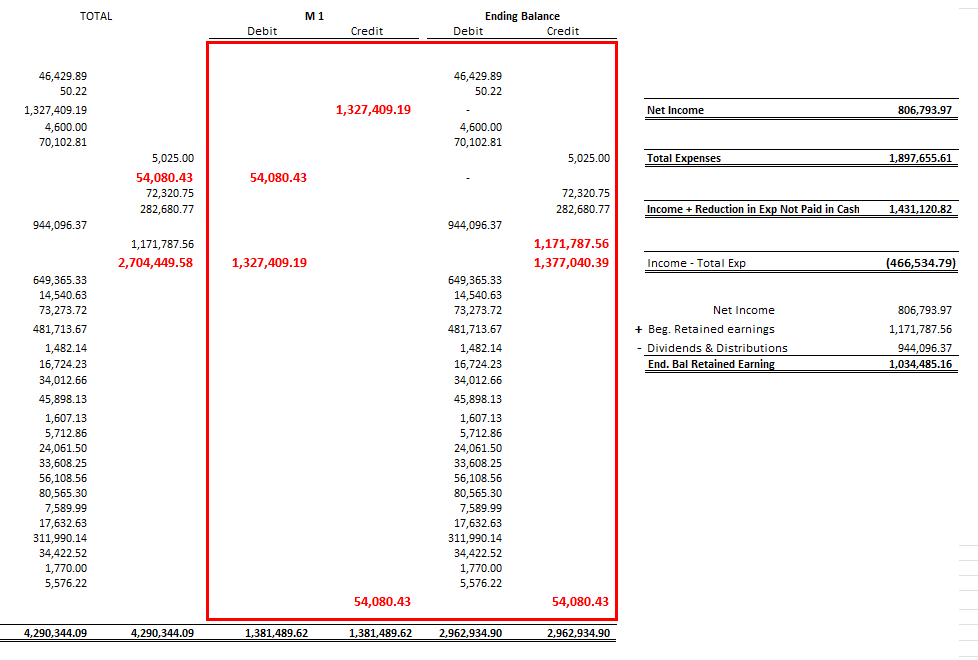

Part 4: Converting from Accrual to Cash Basis on the 1120-S

Accrual accounting records revenue and expenses when they are earned or incurred, no matter when the cash actually moves. Cash accounting recognizes them only when cash changes hands. Moving from accrual to cash means reclassifying transactions so they line up with real cash movements, which zeroes out both receivables and payables.

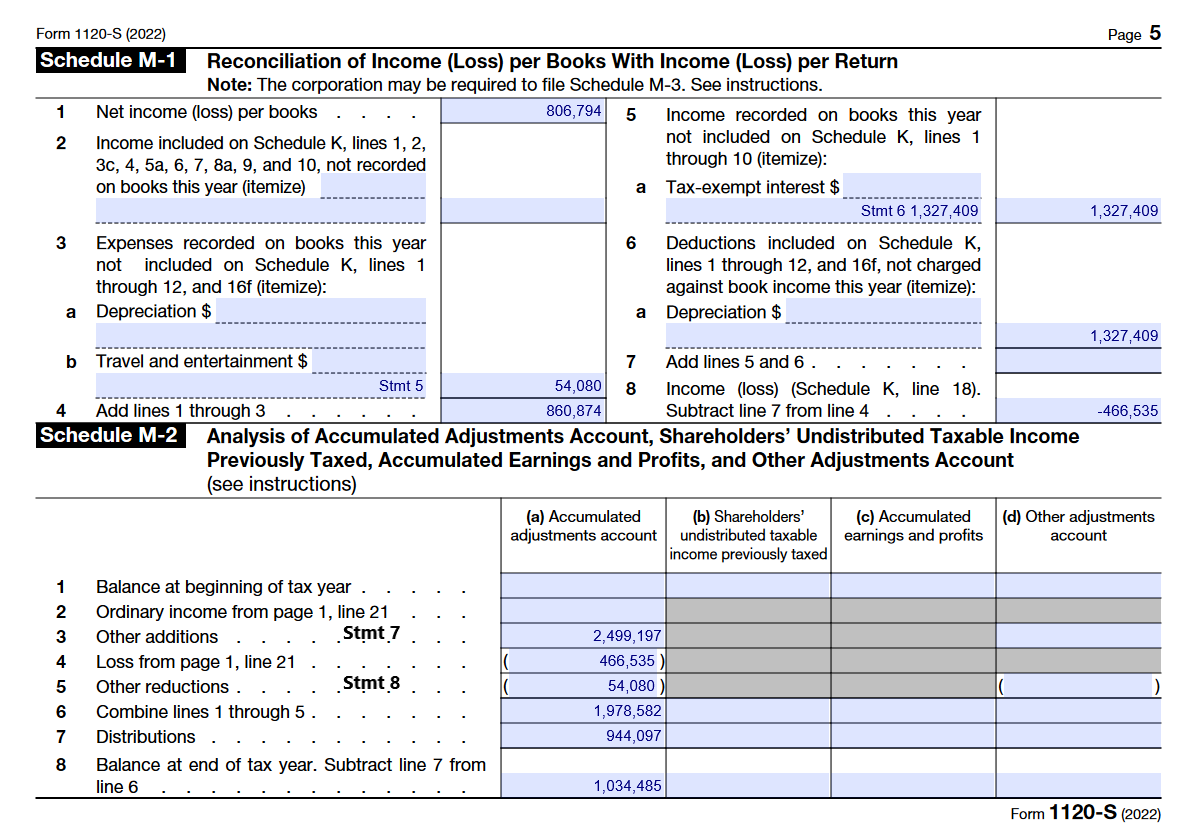

Once you make that shift, the resulting figures from the final balance can be reported on Schedule M-1 of the 1120-S.

So why make the switch from accrual to cash on a 1120-S? A few common reasons:

- Simpler reporting. Cash basis removes much of the complexity of tracking receivables, payables, and the timing differences accrual accounting creates. That is a real help for smaller S-corporations.

- Possible tax advantages. Cash basis can let you defer tax on income until you actually receive it, which can ease cash flow.

- Compliance. Some S-corporations qualify for, or are required to use, cash basis for tax purposes depending on their size or industry.

- Operational fit. If a company mostly deals in cash and straightforward transactions, cash basis matches how it already works.

- Less complexity. Tracking receivables, payables, and inventory gets simpler, which matters most for smaller businesses with limited resources.

In Closing

The adjusted trial balance is a crucial snapshot. It keeps your books accurate and aligned with accounting standards, and for an S-corporation it becomes the foundation for correct tax reporting. The adjustments we walked through, clearing the tax payment, fixing the subsidiary error, combining the entities, and converting to cash basis, show just how closely financial accounting and tax accounting depend on each other. Handled carefully, they lead to cleaner reporting, smoother compliance, and a tax return you can stand behind.

Practice What You Learned

Ready to test your knowledge?

Practice the 1120-S in the Tax Return Workshop