Mastering the Art of Journal Entries: A Complete Guide to Precision Accounting

A clear, step-by-step guide to journal entries and the double-entry system, worked through a full month of real business transactions with debit and credit diagrams.

Journal entries are the foundation of the entire accounting process. They are the first formal record of every financial transaction a business makes, capturing each event in a structured, chronological way before that information flows into the ledger and, eventually, into the financial statements. A solid command of journal entries is the single most valuable skill an accounting student can build, because every report that follows depends on each entry being recorded correctly.

Journal entries, also known as accounting entries or bookkeeping entries, record the financial transactions of a business in the order they occur. These transactions can include sales, purchases, expenses, revenue, asset acquisitions, liabilities, and changes in equity.

Each journal entry contains a few essential pieces of information:

- the date of the transaction,

- the accounts affected,

- the amounts involved,

- and a short description of the transaction's purpose or nature.

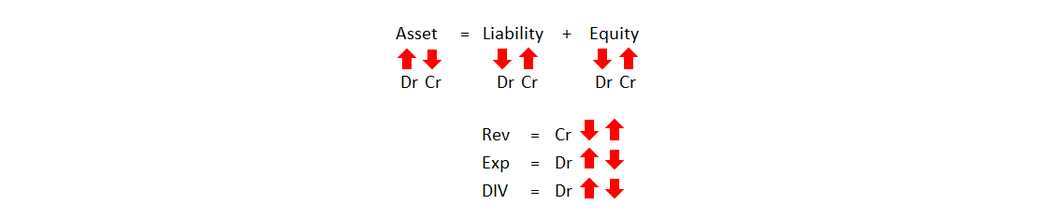

Journal entries are the heart of the double-entry accounting system. Under this system, every transaction affects at least two accounts, with one account debited and another credited by an equal amount, so that the accounting equation always stays in balance:

Assets = Liabilities + Equity

The information recorded in journal entries is later transferred to the general ledger and organized into individual accounts. From there it is used to prepare the financial statements and to support the financial analysis that lets a business monitor performance and make informed decisions.

The Meaning of the Equation

The equation Assets = Liabilities + Equity is the fundamental accounting equation, also known as the Balance Sheet Equation or the Accounting Identity. It represents the core principle of double-entry accounting and gives a snapshot of a company's financial position at a specific point in time. Each component has a precise meaning.

- Assets are the economic resources owned by a business that hold measurable value and are expected to provide future benefit. Assets include cash, accounts receivable, inventory, buildings, equipment, and investments. In short, assets represent everything of value that the business possesses.

- Liabilities are the obligations or debts a business owes to outside parties such as creditors, suppliers, and lenders. Liabilities include accounts payable, loans, bonds, and other obligations the company must repay in the future. They represent the claims that external parties hold against the company's assets.

- Equity, also called Owner's Equity or Shareholders' Equity, is the residual interest in the assets of the business after deducting its liabilities. In other words, equity is what remains for the owners once all debts and obligations have been settled. It can also include retained earnings, the accumulated profits that have not yet been distributed to shareholders.

The accounting equation must always balance, which means the total value of a company's assets always equals the combined total of its liabilities and equity. This balance is what keeps the accounting records accurate and reflects the principle that a company's assets are financed either by outside parties (liabilities) or by the owners themselves (equity).

How Debits and Credits Affect Each Account

Before recording any entry, it helps to fix in mind which side of each account increases and which side decreases.

- Assets increase with a debit and decrease with a credit.

- Liabilities increase with a credit and decrease with a debit.

- Equity increases with a credit and decreases with a debit.

Two further rules follow from how revenue and expenses connect to equity:

- Revenue increases equity, so revenue accounts increase with a credit.

- Expenses and dividends decrease equity, so those accounts increase with a debit.

A useful way to understand the logic: every financial transaction moves economic value from one place to another. Credits represent the source from which value flows, showing where the value is coming from. Debits represent the destination to which value flows, showing where the value is going or being used.

Worked Example: A New Company, Month by Month

The clearest way to learn journal entries is to follow a single business through its first month. Jimmy Connors starts his company, Tennis Tours, to carry customers from New York's JFK Airport to the Flushing Meadows-Corona Park. The company begins operating in March, and the following transactions take place during its first month.

Date: March 1

- Cash: Jimmy invests $10,000 in cash into the company, which is an asset. Assets increase with a debit, so the Cash account is debited by $10,000.

- Van: Jimmy also contributes a van valued at $7,500. The van is also an asset, so the Van account is debited by $7,500.

- Common Shares (Equity): In exchange for the investment, Jimmy receives common shares representing his ownership interest in the business. Equity increases with a credit, so the Common Shares account is credited by $17,500, the combined value of the cash and the van.

This entry records the increase in assets (Cash and Van) on the debit side and the increase in equity (Common Shares) on the credit side, keeping the accounting equation in balance.

Date: March 3

- Advertising Expense: Jimmy spends $1,000 on online advertising. Expenses increase with a debit, so the Advertising Expense account is debited by $1,000 to recognize the cost.

- Cash: Jimmy pays $1,000 in cash. Cash is an asset, and when it is paid out it decreases, so the Cash account is credited by $1,000.

This entry records the expense on the debit side and the reduction of cash on the credit side, reflecting the cash outflow for the advertising cost.

Date: March 5

- Equipment: Jimmy purchases equipment for $3,000. Equipment is an asset, so the Equipment account is debited by $3,000.

- Accounts Payable: Because the purchase is made on account, Jimmy does not pay immediately but agrees to pay in the future. Accounts Payable is a liability, and liabilities increase with a credit, so the Accounts Payable account is credited by $3,000.

This entry shows that the company has acquired an asset while taking on a matching obligation to pay for it later.

Date: March 6

- Van: Jimmy purchases a second van for $8,000. Vans are assets, so the Van account is debited by $8,000.

- Cash: Jimmy pays $2,000 in cash toward the van. Cash decreases when used for payment, so the Cash account is credited by $2,000.

- Notes Payable (Car Loan): To cover the remaining $6,000, Jimmy takes out a car loan. This is a liability, so the Notes Payable account is credited by $6,000.

This entry reflects one asset increasing (the van), another asset decreasing (cash), and a liability increasing (the loan). It shows how a single purchase can be financed by a mix of cash and borrowing.

Date: March 15

- Cash: The first tour group has thirteen customers, twelve of whom pay $1,000 each at the time of the tour. The $12,000 collected is an asset, so the Cash account is debited by $12,000.

- Accounts Receivable: One customer is unable to pay at the time of the tour but promises to pay by the end of the month. This promise is a receivable, an asset, so the Accounts Receivable account is debited by $1,000.

- Service Revenue: The tour has been provided, so the full $13,000 is earned revenue regardless of when each customer pays. Revenue increases with a credit, so the Service Revenue account is credited by $13,000.

This entry records the cash collected, the amount still owed by one customer, and the full revenue earned from delivering the tour.

Date: March 16

- Salaries Expense: Jimmy pays his employees' salaries of $3,000, an operating expense. Expenses increase with a debit, so the Salaries Expense account is debited by $3,000.

- Cash: The salaries are paid from the company's cash, so the Cash account is credited by $3,000.

This entry records the cost of paying employees on the debit side and the cash outflow on the credit side.

Date: March 17

- Fuel Expense: Jimmy purchases $500 of fuel for the vehicles, an operating expense directly related to running the vans. The Fuel Expense account is debited by $500.

- Cash: The fuel is paid for in cash, so the Cash account is credited by $500.

This entry records the fuel cost on the debit side and the matching cash outflow on the credit side.

Date: March 19

- Van: Jimmy pays $800 to repair a broken window on one of the vans. In this example the cost is treated as a capitalized addition to the asset's value, so the Van account is debited by $800.

- Cash: The repair is paid from the company's cash, so the Cash account is credited by $800.

This entry records the increase in the van's recorded value on the debit side and the cash outflow on the credit side.

Date: March 20

- Accounts Payable: On March 5, Jimmy purchased equipment on account, creating a $3,000 liability. He now settles that liability. Accounts Payable decreases when paid, and a liability decreases with a debit, so the Accounts Payable account is debited by $3,000.

- Cash: The payment is made in cash, so the Cash account is credited by $3,000.

This entry records the reduction of the liability on the debit side and the cash used to settle it on the credit side.

Date: March 22

- Utilities Expense: Jimmy receives a utility bill for $200. Utilities expense covers services such as electricity, water, and gas used in the business. The Utilities Expense account is debited by $200 to recognize the cost.

- Accounts Payable: Because the bill has been received but not yet paid, it creates an obligation to pay in the future. The Accounts Payable account is credited by $200.

This entry recognizes the expense on the debit side and the new liability on the credit side. The payment will be made later when the bill is settled.

Date: March 25

- Cash: Jimmy receives the final $1,000 from the customer who had promised to pay for the March 15 tour. Cash increases, so the Cash account is debited by $1,000.

- Accounts Receivable: The amount previously recorded as a receivable is now collected, so it is reduced. The Accounts Receivable account is credited by $1,000.

This entry records the cash received on the debit side and the reduction of the outstanding receivable on the credit side, completing the collection from the March 15 tour.

Date: March 31

- Cash: Jimmy runs a second tour for a group of fifteen people, each paying $1,000, for a total of $15,000. The cash collected is an asset, so the Cash account is debited by $15,000.

- Service Revenue: The tour has been delivered, so the $15,000 is earned. Revenue increases with a credit, so the Service Revenue account is credited by $15,000.

This entry records the cash received on the debit side and the revenue earned from the second tour on the credit side.

Date: March 31

- Salaries Expense: Jimmy again pays his employees' salaries of $3,000, an operating expense, so the Salaries Expense account is debited by $3,000.

- Cash: The salaries are paid in cash, so the Cash account is credited by $3,000.

This entry records the cost of paying employees on the debit side and the cash outflow on the credit side.

Date: March 31

- Retained Earnings: A cash dividend is a distribution of profits to shareholders. Equity decreases with a debit, so the Retained Earnings account is debited by $5,000 to reflect the distribution.

- Cash: The dividend is paid in cash, so the Cash account is credited by $5,000.

This entry records the reduction in equity on the debit side and the cash used to pay the dividend on the credit side.

Bringing It Together

Each of these entries follows the same discipline. Two or more accounts move, the debits equal the credits, and the accounting equation stays in balance. Once recorded, these entries are posted to the general ledger, where they are summarized and used to build the Income Statement, the Balance Sheet, and the Statement of Cash Flows. Master the entry, and every statement that follows becomes far easier to understand.

The fastest way to build that mastery is steady practice with immediate feedback. Work through fresh journal entry problems and get instant, detailed explanations on every answer in the Chapter 1 practice on iLove-Accounting.com.